SG 1.3 Gas rent and mineral property rights

|

|

Leader |

Scope and purposes

The literature is rich in the development of models designed to maximise the intake of governments, where much of the art is related to the creation of an attractive atmosphere for business which will actually develop a win-win situation for governments and serious investors.

There are basically two fiscal regimes of relevance.

In the concession regime, the investor sells the production for a price, deducts costs, pays taxes and keeps what is left to himself.

In the sharing regime, however, the operator receives part of the oil produced as a compensation for his costs, and another part of the production is passed on to him as a payment for his services, after taxes.

Service, buy-back and transfer of rights contracts are also possible, but more rare.

As to the fiscal instruments, a large arsenal is readily available for policy makers. Usually a mixture of them is used, including signature bonuses, royalties and taxes on profits of varied nature, such as the resource rent taxes of Australia. Even the obligation of acquiring goods and services in the local market can be considered as a form of taxation.

The exploration, development and production of gas reserves seem to require a differentiated treatment from governments, which must ensure a proper balance of risks and rewards to promote the development of their projects. Conditions may vary dramatically from associated to non-associated gas, or if an NOC is included or not in the model.

This study group will compare the solutions adopted by a number of countries, and the results obtained by them.

Topics of interest include

- Identification of regulatory tendencies;

- Assessment of business models for exploration and production of gas;

- Critical analyses of fiscal instruments;

- Development of upstream policies for gas rent.

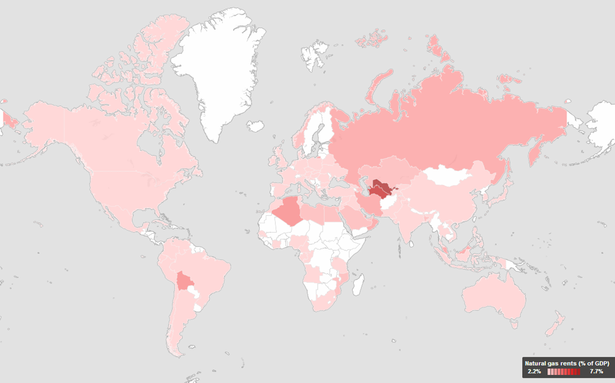

Map and data from World Bank

Members

| Name | Organisation | Country |

| Decio Barbosa | IBP | Brazil |

| Luiz Cezar Quintans | G. Ivo Advogados | Brazil |

| Marcos de Freitas Sugaya | Petrobras | Brazil |

| Wang Guangjun | Petrochina | China |

| Liliane Wietzerbin | GDF Suez | France |

| Vincent Trocme | GDF Suez | France |

| Masoud Hassani | NIGC | Iran |

| Ikhyun Park | Kogas | Korea |

| Kyungsick Park | Kogas | Korea |

| Taehyeong Lee | Kogas | Korea |

| Zainal Abidin Zainudin | Petronas | Malaysia |

| Pawel Jagosiak | PGNiG | Poland |

| Alexey Semenov | Gazprom | Russian Federation |

| Oleg Borodionkov | Gazprom | Russian Federation |

| Guadalupe Vargas Giraldo | Repsol | Spain |

Best practices proposal

This study group is highly interested in the establishment of best practices that will help the industry, policy makers and regulators in securing a reliable and affordable supply of natural gas to the consumers. Some of them are under discussion as follows:

- Reduce the relative importance of signature bonuses and area retention fees in the bidding processes;

- Increase the relative importance of exploratory programmes, domestic content and other instruments that can harness economic and social development;

- Promote a good assessment of the actual capability of local suppliers for equipments and services beforehand, and consider realistic mechanisms to account for the individual items that compose the requirements of domestic content, allowing companies to demonstrate higher than expected costs;

- Replace flat royalty rates and other instruments based on production or income revenue by progressive mechanisms based on profits, or consider the use of progressive royalty rates;

- Allow the depreciation of assets before production starts, and consider the use of generous uplift allowances that will not cause gold platting, especially for unconventional gas and production in frontier locations;

- For marginal fields, consider a reduction of royalty rates and other mechanisms that will allow efficient operators to maintain production, employment and tax collection;

- Whenever possible, consider ring fencing as a means to create equal opportunities and protect the government share;

- For the production of unconventional gas, consider the concession of fiscal incentives to compensate for the higher costs.

Key literature

Kellas G., Natural gas: Experience and issues in Daniel et al. (eds.), The Taxation of Petroleum and Minerals: Principles, Problems and Practice, pp.163-183, 2010.

Ernst & Young, Global oil and gas tax guide, 2012.

Javid S., Harnessing the potential of the UK’s natural resources: a fiscal regime for shale gas, HM Treasury, July 2013.

Return to WOC 1: Exploration and Production